☁ Diving into RPO Metrics

What is Driving $NOW cRPO Movements?

Welcome to Hard Mode! Top founders, VCs, and investors subscribe for insights and analysis to successfully compete and invest in the Enterprise SaaS market. If you haven’t subscribed yet, we love to make new friends 👇

🐇 Bookings vs. RPO Rabbit Hole

What started off as a “quick” Friday project of creating a ServiceNow Q4 earnings thread, quickly led me down the metrics rabbit hole of bookings, RPO, and revenue forecasting.

Piecing everything together is simple, but not easy. In a beautiful (impossible) vacuum, all these metrics mesh 1-to-1 and an analyst could forecast revenue perfectly.

In reality, the messiness of a B2B SaaS GTM machine along with the limitations of public data makes this far from friendly.

But that’s where the fun starts.

In this piece we’ll cover:

Internal vs. public booking metrics

How different business decisions can lead to incorrect public assumptions

How these impacts might impact different forecasting methodologies

Importance of the CFO org understanding how public metrics will be interpreted

☕ I would highly suggest you have your morning coffee before reading this 😉

Bookings Metrics 101

There’s a few key terms and concepts we’re going to walk through and bridge here:

ACV. How much new annual recurring business is closed by the organization.

TCV (Total Contract Value). Typically the ACV x number of years contracted.

Renewal Rates. How much ACV up for renewal is renewed in the period.

Bookings. How much business (new + renewal) a company closes in a period. Should equal TCV.

Billings. How much an organization actually bills it’s customers in a period.

RPO (Remaining Performance Obligation). How much total contracted revenue has yet to be recognized (TCV - rev rec to date). The derivative Current Remaining Performance Obligation (cRPO) measures what is contracted and yet to be recognized for only the next 12 months.

Deferred Revenue. Of the total amount billed, how much revenue has yet to be recognized.

Through this whole process we’re trying to convert a long list of contracts with messy terms to get to a methodology to forecast revenue and cash flow. The holy grail would be to accurately forecast active ARR at spot rates, but that’s nearly impossible with public data unless it’s disclosed.

We focus primarily on revenue metrics in this piece, if you would like to learn more about FCF:

Operationally, any time a contract is closed, accounting will create a revenue and billings schedule which then flows to the different publicly disclosed GAAP and non-GAAP metrics.

Individual contracts will have a number of moving pieces:

Annual contact value

Total contract value (including terms which may ramp through contract)

Billings terms

External metrics can also be impacted by the additional timing complexities within large GTM organizations:

Allowing pull forward of renewals

Stub billings periods

Changing frequency/size of contracts with different rev rec, billings, and ARR terms

Here are a number of scenarios and how different contract terms might impact external metrics.

Example 1: An AE closes a 1 year, $100 contract with annual upfront billings on Day 1 of the quarter

Revenue is recognized ratably through the period.

As this is a one year contract with matching billing, RPO, cRPO and Deferred Revenue all match.

At the end of the year, all revenue has been recognized so the accounts are equal to 0

Example 2: An AE closes a 2 year, $200 TCV contract with annual upfront billings on Day 1 of the quarter

Revenue is still recognized ratably over a 2 year period

In this scenario, RPO reflects the full TCV of the contract, cRPO captures the forward, rolling 12-month contracted rev rec, and deferred revenue fluctuates based on the 2 billings dates

You’re starting to see how these metrics can start to diverge quickly

Example 3: 18-month contract with 6-month stub billings

In some cases, customers want a stub billing period to get back to a normalized billing cycle.

In this scenario we assume 2 billing periods in an 18-month contract. One for 6 months and second for 12 months.

In this case, you start to see Y1 billings below ACV. Using only deferred revenue would lead analysts to underestimate ARR and using only RPO would over estimate cash collection in the period.

This can wash the other way if you bill for 18 months up front (or longer).

Example 4: Renewal and expansion ACV gets pulled forward to earlier quarter

🔥 Ok, now we’re getting spicy

Timing changes can start to wreak havoc on externally calculated metrics

Pulling forward expansion contracts is fairly common in sales organizations. Customers can be offered preferred pricing to lock in their new business earlier than expected.

In many cases, this is a win-win and if this percentage is fairly similar across periods, then the impact will generally wash out.

However if this accelerates or decelerates unexpectedly it can cause analysts to overestimate or underestimate your in-period performance and/or create comp issues in future periods.

In times of uncertainty this delta can swing either way. It might be easier for AEs to reach quota by pulling forward an expansion deal than close a new customer. On the flipside, customers may hesitate to expand contracts until they are more certain of their budgets and needs.

Next, we will see how this mechanic led ServiceNow to miss their cRPO guidance this past quarter.

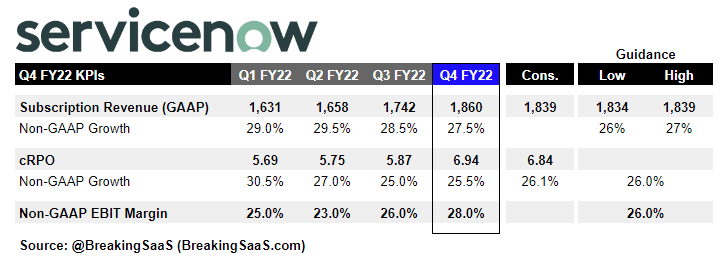

ServiceNow Case Study

ServiceNow reported Q4 and FY22 results on January 25th and many analyst questions focused on the cRPO miss vs. guidance which management was clear to call out was impacted by a lower percentage of early renewals vs. prior Q4s.

Thankfully you’re an RPO pro now and can decipher what that means.

Let’s look at the results.

NOTE: I’m swagging FX in all this. If you have a good idea how to model here would love to chat.

ServiceNow Q4 non-GAAP cRPO grew 25.5% YoY, just shy of 26% YoY guidance:

All else equal, lower cRPO = lower calculated bookings = lower implied net new ACV = a headwind to future growth. Not to mention could signal a lower growth trajectory in the forecast period.

In the example below, you can see how these results might playout across market participants. Again, FX makes this messy and I make some high level assumptions to try to convert CC growth to reported for calculation purposes.

A small miss to guidance for a popular stock would likely suggest a much larger miss to the “buyside” which expects management to beat guidance and consensus.

Note: I do not know what the buyside was actually expecting for these metrics.

But diving deeper, bookings are really comprised of 4 components:

New customer bookings (revenue impact)

Expansion bookings (revenue impact)

Renewal bookings (revenue impact)

Early renewal bookings (timing, little/no revenue impact)

ServiceNow CFO, Gina Mastantuono, gave additional color on how each of these components impacted the cRPO growth vs. company guidance and how the primary driver (timing) was not a revenue impact:

On a constant currency basis, growth was 25.5%. While constant currency cRPO growth came in just shy of our guidance of 26%, we actually outperformed our target for net new ACV and renewal ACV for contracts expiring in the quarter. The delta came from fewer early 2023 renewals than is typical in the fourth quarter. Given our strong renewal rates, which remain the best-in-class 98% in Q4, this is only a timing issue. We expect these customers to ultimately renew upon contract expirations, providing opportunities to drive further expansion throughout 2023. The timing of early renewals does not impact 2023 subscription revenue growth, only RPO. Net new ACV would drive incremental revenue growth, and there, we exceeded our forecast. Our larger-than-average Q4 customer cohort not only renewed at a very strong rate, net expansion also remained robust. What's more, the strength in net new ACV wasn't limited to existing customers. New customer net new ACV grew over 30%.

When asked a follow up question on cRPO growth and the economic environment, Gina noted this timing behavior shift would be expected in an uncertain environment and reiterated how net new ACV (revenue drivers) actually outperformed:

So I think what you're seeing is early renewals were always correlated and still always correlated to net new ACV. And when people early renew, it's really about co-terming multiple contracts. And certainly, in the current environment, I don't know if you want to say it's less budget flush or just more tightening of budgets, the need or the desire to co-term the contract is a little bit less than what we've seen historically, not altogether surprising given the current macro. It's why I wanted to be really clear about the fact that early renewals have no impact on future revenue, right? And in the quarter, our target forecast for net new ACV as well as renewal ACV within the quarter actually overachieved, which is why we were able to come out with a strong 2023 revenue guide and why we feel good about not only the Q4 results, but also the position that we stand in the market as well entering 2023.

All these comments suggest the miss was generated by timing and not an incremental revenue concern. Backing up these comments, management provided guidance above consensus:

Net / Net

For external analysts, it’s important to be aware how changing business dynamics can impact external metric calculations and lead to forecasting errors.

Further, analysts need to incorporate both RPO and deferred revenue in their calculations to accurately forecast Revenue and Cash Flow.

Finally, CFOs and finance teams need to be aware how external metrics will be used by market participants to understand results and forecast future performance.

Finance, GTM and Sales all need to be aligned how different incentives and sales processes will impact external metrics and be prepared to discuss why and how those decisions are impacting performance.

If you would like to learn more about SaaS FCF:

With Blessings of Strong NRR,

Thomas

Got to understand accounting to know how it all works together

While reading Servicenow's transcript I wondered where I could find a detailed explanation on the early renewals. Here we are.

Great job Thomas!